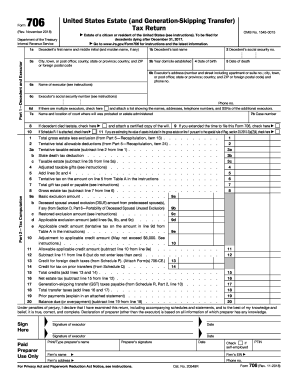

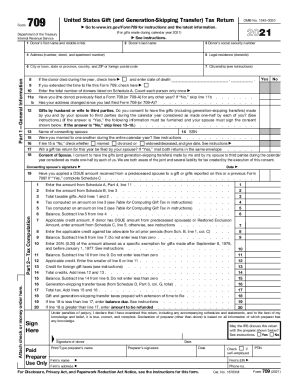

IRS 706 2019-2024 free printable template

Show details

40. Enter here and on Schedule R Part 2 line 9. SCHEDULE R-1 Form 706 Payment Voucher Executor File one copy with Form 706 and send two copies to the fiduciary. 8. Fiduciary Check here if this Schedule PC is being filed with the original Form 706 or is being filed by the same fiduciary who filed the original Form 706 for decedent s estate. Daytime telephone number 7. Number of Claims. Enter number of Schedules PC being filed with Form 706. Each separate claim or expense requires a separate...

pdfFiller is not affiliated with IRS

Get, Create, Make and Sign

Edit your irs form 706 2019-2024 form online

Type text, complete fillable fields, insert images, highlight or blackout data for discretion, add comments, and more.

Add your legally-binding signature

Draw or type your signature, upload a signature image, or capture it with your digital camera.

Share your form instantly

Email, fax, or share your irs form 706 2019-2024 form via URL. You can also download, print, or export forms to your preferred cloud storage service.

Editing irs form 706 online

To use the professional PDF editor, follow these steps:

1

Check your account. In case you're new, it's time to start your free trial.

2

Prepare a file. Use the Add New button. Then upload your file to the system from your device, importing it from internal mail, the cloud, or by adding its URL.

3

Edit form 706. Rearrange and rotate pages, add new and changed texts, add new objects, and use other useful tools. When you're done, click Done. You can use the Documents tab to merge, split, lock, or unlock your files.

4

Get your file. Select the name of your file in the docs list and choose your preferred exporting method. You can download it as a PDF, save it in another format, send it by email, or transfer it to the cloud.

pdfFiller makes dealing with documents a breeze. Create an account to find out!

IRS 706 Form Versions

Version

Form Popularity

Fillable & printabley

How to fill out irs form 706 2019-2024

How to fill out form 706:

01

Make sure to gather all necessary information and documents, such as the decedent's personal information, assets, and liabilities.

02

Begin by filling out Part 1 of the form, which includes basic information about the decedent and the estate.

03

Proceed to Part 2, where you will report the decedent's gross estate. This involves listing all assets, including real estate, bank accounts, investments, and personal property.

04

Following Part 2, complete Part 3 to calculate the allowable deductions from the gross estate. This may include funeral expenses, administrative expenses, and property that qualifies for the marital or charitable deductions.

05

Move on to Part 4, where you will calculate the taxable estate by subtracting the allowable deductions from the gross estate.

06

Next, complete Parts 5 and 6 to determine the federal estate tax by applying the applicable tax rates and credits to the taxable estate.

07

Once all calculations are completed, fill out Part 7 to report any prior transfers made by the decedent that could affect the estate tax.

08

Finally, review the form for accuracy and sign it before submitting it according to the instructions provided.

Who needs form 706:

01

Form 706 is required to be filed by the executor or administrator of a deceased individual's estate if the decedent's gross estate, plus adjusted taxable gifts and specific exemptions, exceeds the amount set by the IRS.

02

It is also required in cases where a surviving spouse wants to make use of any unused portion of the decedent's estate tax exemption.

03

Additionally, even if the filing of Form 706 is not mandatory, it may be beneficial to file it voluntarily in order to establish the value of the estate and establish a new basis for the assets being inherited.

Video instructions and help with filling out and completing irs form 706

Instructions and Help about irs form 706 fillable pdf

My name is Jim Baker from the biggest accidents and I just had an interesting case this week a non-resident who owned in a house in Florida passed away and if you're not aware of it there is an estate tax for what is in a state tax for everyone but for non-residents the exemption is only sixty thousand dollars for residents for you and me and people that live here a residents and citizens of the US they state tax exemptions five million dollars, so you don't have to file now about pay anything unless you're a state and all your assets are worth over five million dollars when you die but for a non-resident if you are from Chile or from Brussels and you have a house here, and it's worth more than sixty thousand dollars, and it's not held in any kind of entity, or you just own it there's an estate tax to pay when you die this there should be some planning that goes into this before you actually before you buy the property, and before you die but regardless Rihanna pretend no planning was done, and I'm just going to go over...

Fill estate tax return : Try Risk Free

People Also Ask about irs form 706

What is the penalty for not filing form 706?

What is the deadline to file a 706?

What is form 706 used for?

Who must file a 706 tax return?

When must a form 706 be filed?

Does a Form 706 have to be filed?

For pdfFiller’s FAQs

Below is a list of the most common customer questions. If you can’t find an answer to your question, please don’t hesitate to reach out to us.

What is form 706?

Form 706 is the U.S. Estate Tax Return, used to report the value of a decedent's estate and calculate the federal estate tax. The form is filed with the Internal Revenue Service (IRS) by the executor of the estate.

What is the purpose of form 706?

Form 706 is used to report the estate taxes that are due from an estate of a deceased person. The estate tax is paid by the estate itself, not the beneficiaries. Form 706 is used to report the value of the estate, including the net estate, any deductions, and the tax due. It also provides information to the IRS about the assets and liabilities of the estate.

What is the penalty for the late filing of form 706?

The penalty for late filing of Form 706 is $10 for each month or part of a month that the return is late, up to a maximum of 25% of the amount of the tax due.

Who is required to file form 706?

Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is required to be filed by the executor or administrator of a decedent's estate. It is filed to report and pay any estate tax owed to the Internal Revenue Service (IRS) when the value of the decedent's estate exceeds the applicable federal estate tax exemption amount.

How to fill out form 706?

Form 706 is a tax form that is used to calculate and report estate taxes for individuals who have passed away. Filling out this form can be complex and it is recommended to seek the assistance of a tax professional or estate planning attorney. However, here are the general steps to fill out Form 706:

1. Gather all necessary information and documents: You will need the deceased person's personal information, such as their full name, Social Security number, and date of birth. Additionally, you will need the details of their assets, including real estate, bank accounts, investments, and life insurance policies.

2. Determine the estate's gross value: Calculate the total value of the assets as of the date of the decedent's death. This includes the fair market value of all assets, including cash, stocks, bonds, real estate, business interests, insurance proceeds, and other assets.

3. Subtract allowable deductions: Calculate any allowable deductions based on the instructions provided on the form. This may include funeral expenses, debts owed by the deceased, and certain administrative expenses.

4. Calculate the net estate value: Subtract the allowable deductions from the gross value to determine the net estate value.

5. Determine the unified credit: Calculate the unified credit available for the estate. This credit allows for a certain amount of the estate's value to be exempt from estate taxes. The unified credit amount may vary each year, so refer to the instructions for the specific year in question.

6. Calculate the estate tax: Calculate the estate tax owed by multiplying the remaining net estate value (after deducting the unified credit) by the applicable tax rate. Again, refer to the instructions for the specific year in question for the tax rate.

7. Complete the remaining sections of the form: Provide information about the decedent's spouse, any other beneficiaries, gifts made during their lifetime, and any previous tax filings or payments made.

8. Sign and submit the form: Sign the completed form and any associated schedules, and submit it to the Internal Revenue Service (IRS) along with any required supporting documents by the deadline. Be sure to keep a copy of the form and supporting documents for your records.

Keep in mind that these steps are a general guide, and it is advised to seek professional assistance to ensure accurate completion of Form 706, as estate tax laws can be complex and subject to change.

What information must be reported on form 706?

Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return, is used to report the value of an individual's estate and calculate any estate tax owed. The following information must be reported on Form 706:

1. Personal Information: The decedent's name, Social Security number, date of death, and address.

2. Executor Information: The name, mailing address, and contact information of the executor or personal representative handling the estate.

3. Gross Estate: The total value of the decedent's assets at the time of their death, including real estate, bank accounts, investments, business interests, and personal property. This section requires a detailed list of each asset, its fair market value, and any debts or liabilities associated with it.

4. Deductions: Certain deductions can be claimed to reduce the gross estate, such as funeral expenses, administrative expenses, debts, mortgages, and casualty losses.

5. Taxable Estate: The taxable estate is calculated by subtracting the allowed deductions from the gross estate value. This amount is then used to determine the estate tax liability.

6. Gifts and Prior Transfers: Information regarding any gifts made by the decedent during their lifetime that exceeded the annual gift tax exclusion. This includes gifts made within three years of death and any gift or inheritance tax paid.

7. Generation-Skipping Transfers: Information on any transfers made to skip persons, such as grandchildren or non-relatives, during the decedent's lifetime or at death. Certain exemptions and exclusions may apply.

8. Tax Computation: This section calculates the total estate tax owed based on the taxable estate and applies credits or exemptions available under the tax laws.

9. Payment and Refund: Information on the payment of any estate tax due or requesting a refund if excess tax was paid.

10. Signatures: The return must be signed by the executor or other authorized individuals, with supporting documentation attached.

It is important to note that the information required on Form 706 may vary depending on the specific circumstances of the estate and any applicable tax laws and regulations. It is recommended to consult a qualified estate tax professional or tax attorney for assistance in completing Form 706 accurately.

When is the deadline to file form 706 in 2023?

The deadline to file Form 706 (United States Estate (and Generation-Skipping Transfer) Tax Return) in 2023 is usually nine months after the date of the decedent's death. However, it is always advisable to consult the Internal Revenue Service (IRS) or a tax professional for the most accurate and up-to-date information regarding deadlines and specific requirements.

How can I edit irs form 706 from Google Drive?

By integrating pdfFiller with Google Docs, you can streamline your document workflows and produce fillable forms that can be stored directly in Google Drive. Using the connection, you will be able to create, change, and eSign documents, including form 706, all without having to leave Google Drive. Add pdfFiller's features to Google Drive and you'll be able to handle your documents more effectively from any device with an internet connection.

How do I edit form 706 1999 online?

pdfFiller allows you to edit not only the content of your files, but also the quantity and sequence of the pages. Upload your 706 to the editor and make adjustments in a matter of seconds. Text in PDFs may be blacked out, typed in, and erased using the editor. You may also include photos, sticky notes, and text boxes, among other things.

How can I edit 706 form on a smartphone?

The easiest way to edit documents on a mobile device is using pdfFiller’s mobile-native apps for iOS and Android. You can download those from the Apple Store and Google Play, respectively. You can learn more about the apps here. Install and log in to the application to start editing 706 form.

Fill out your irs form 706 2019-2024 online with pdfFiller!

pdfFiller is an end-to-end solution for managing, creating, and editing documents and forms in the cloud. Save time and hassle by preparing your tax forms online.

Form 706 1999 is not the form you're looking for?Search for another form here.

Keywords relevant to form 706 estate tax return

Related to 1999 form 706

If you believe that this page should be taken down, please follow our DMCA take down process

here

.